Luxury’s Market Divide Deepens as Hermès Outperforms and Kering Seeks Stability While Moncler Holds Steady

Luxury’s pendulum swings, but Hermès, as usual, seems immune to gravity. The House delivered an 18% surge in fourth-quarter sales, closing out 2024 with a bang while much of the sector continues to grapple with declining demand. With total revenues hitting €4 billion in Q4, Hermès continues to operate in a league of its own, unfazed by the hurdles that have tripped up LVMH and Kering, which posted a meager 1% increase and a 12% decline, respectively.

What’s driving the brand’s seemingly unstoppable momentum? For one, strategic expansion paid off handsomely. The Middle East emerged as a key growth driver, with an astonishing 123.2% increase, fueled by Hermès’ acquisition of its UAE retail network. The Americas followed suit with a 22.3% uptick, boosted by well-timed store openings in Atlanta and Princeton, while Europe (excluding France) posted a healthy 20.7% climb. Even in a challenging Chinese market, where competitors have struggled to regain momentum, Hermès saw a 7% increase in Asia (excluding Japan).

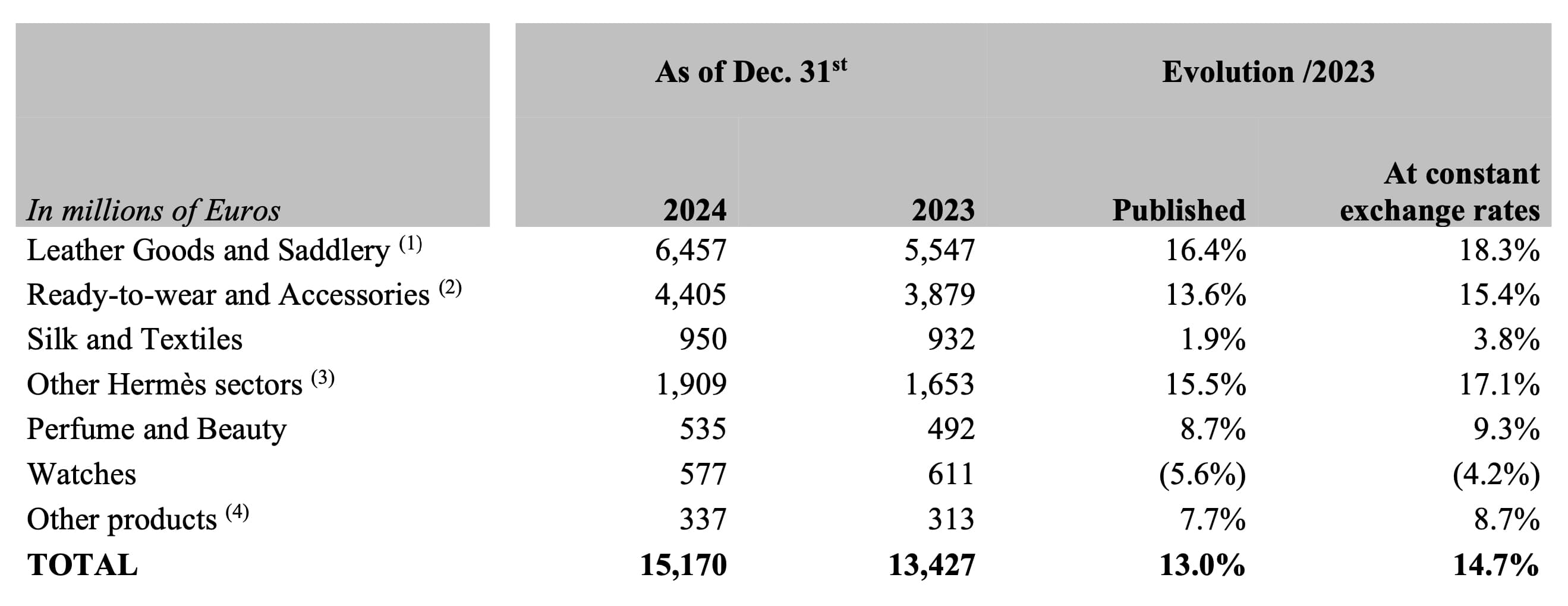

Of course, the House’s signature handbags remain its crown jewel. The leather goods division, home to the Birkin and Kelly, soared 21.5%, reinforcing the timeless appeal of its handcrafted exclusivity. Meanwhile, ready-to-wear and accessories also impressed with a 17% gain. In an era where price hikes and shifting consumer sentiment have left many luxury players treading carefully, Hermès’ playbook—patience, craftsmanship, and scarcity—continues to pay dividends.

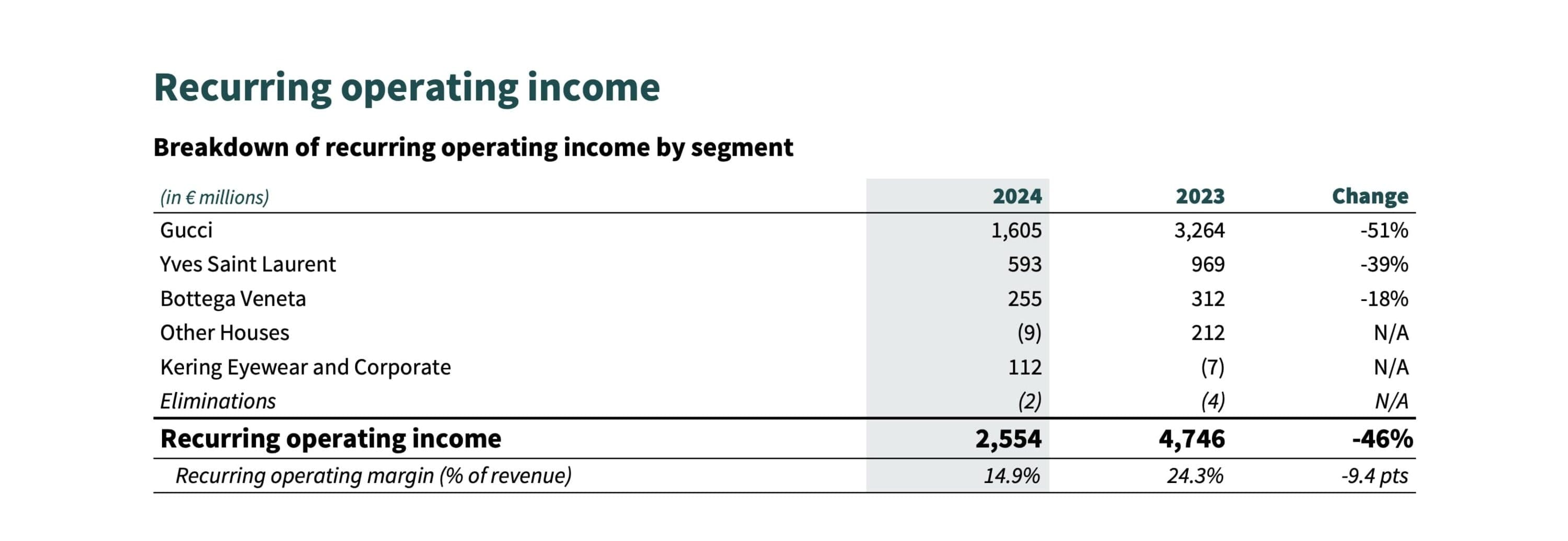

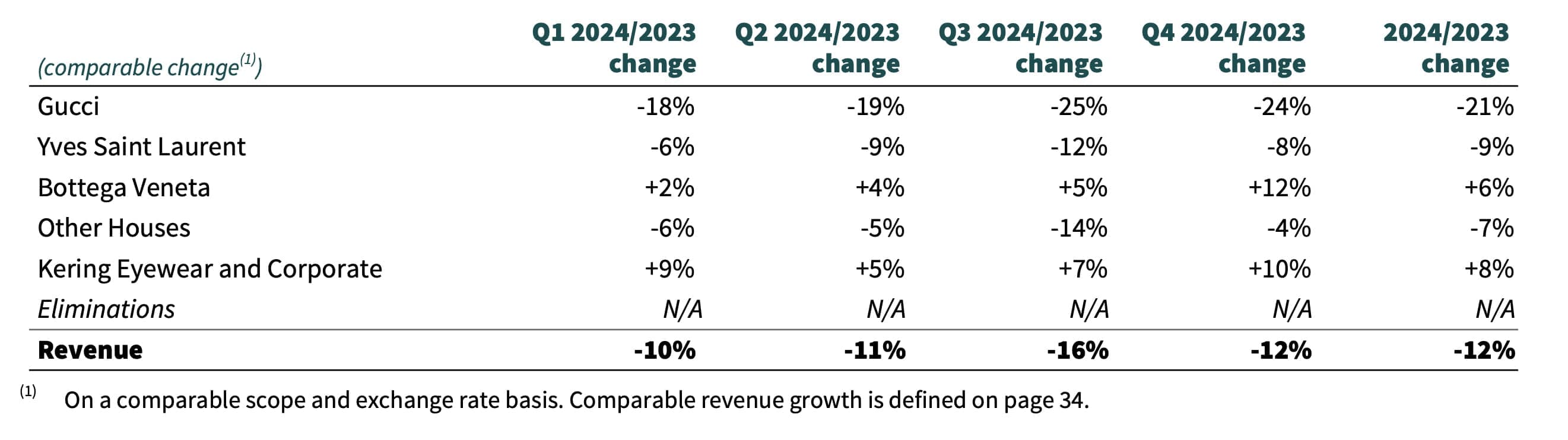

Meanwhile, across the sector, Kering has found itself in rougher waters. The group reported a 12% drop in fourth-quarter revenue, landing at €4.39 billion, a number that, while still grim, beat expectations. But the bigger issue lies in Gucci, Kering’s primary engine, which clocked in a concerning 24% slide in organic sales—missing estimates and underscoring deeper struggles. The House’s future remains uncertain, especially following the abrupt departure of creative director Sabato De Sarno last week. With no successor named and the brand still in search of a clear creative and commercial direction, it’s a pivotal moment for the once-unstoppable Gucci.

Moncler, on the other hand, managed to navigate the choppy waters of 2024 with a steady hand. The Moncler Group surpassed €3.1 billion in annual revenue, marking a 4% increase—7% at constant exchange rates. The Moncler brand itself climbed 5%, proving its resilience in an evolving luxury landscape, while Stone Island saw a 2% decline for the year. However, the fourth quarter brought a 10% revenue boost for Stone Island, hinting that its repositioning strategy might be gaining traction. Notably, Moncler saw solid gains in China, a region that’s posed significant challenges for others in the industry.

As the numbers roll in, one thing is clear—luxury’s winners and losers are being defined by more than just heritage and brand prestige. Strategic expansion, disciplined execution, and a strong creative vision remain essential to weathering the ongoing shifts in consumer sentiment. With Paris Fashion Week around the corner and new leadership needed at some of fashion’s biggest houses, 2025 is shaping up to be a year of big bets, big risks, and even bigger scrutiny. Here’s hoping the industry is ready to play the long game.

Warm Regards,

Kenneth Richard

Chief Impressionist

The Impression