Stable Organic Performance And Strength Beyond Gucci Suggest The Group’s Turnaround Is Quietly Underway

Kering is not back yet—but for the first time in a while, it may be finding its balance.

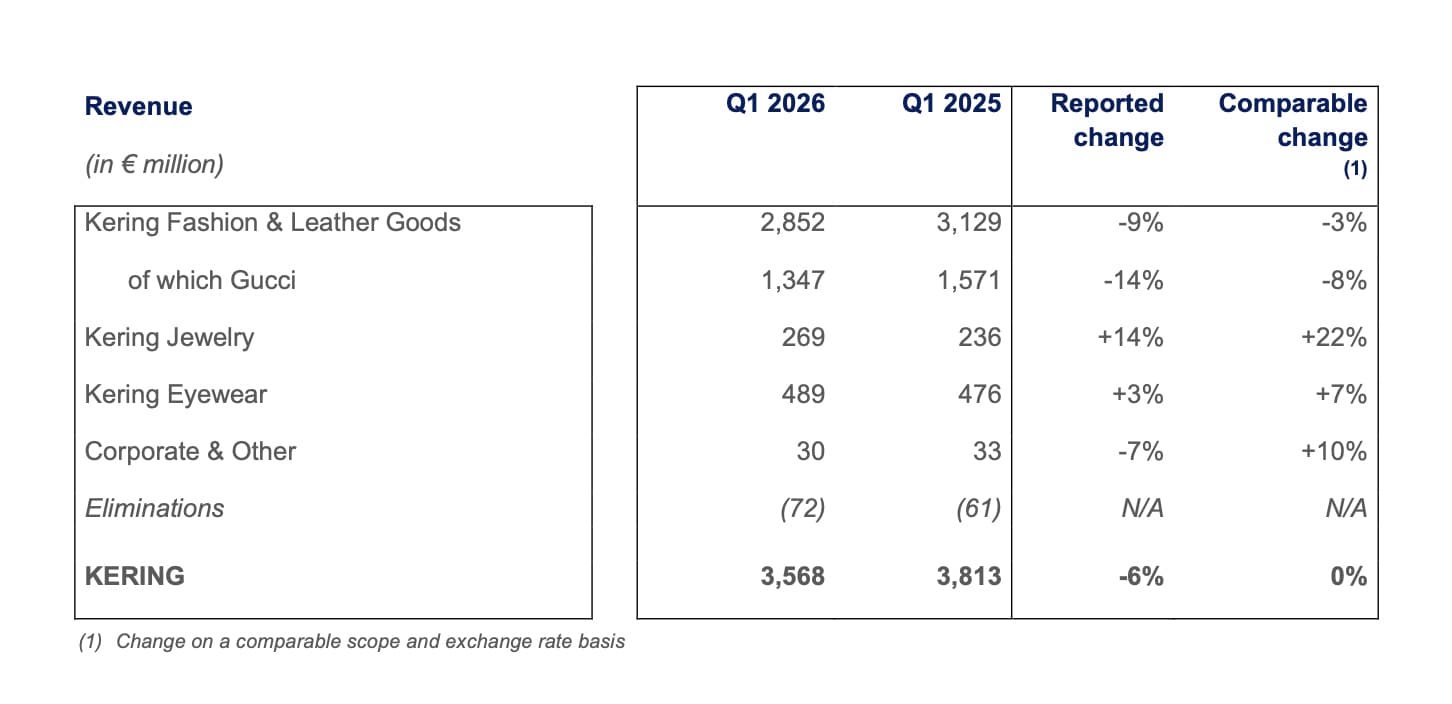

The group reported first-quarter 2026 revenues of €3.57 billion, down 6 percent on a reported basis but stable on a comparable one, a result CEO Luca de Meo framed as “an important first step in our recovery and a further sequential improvement.” After several quarters of consistent declines, stability itself becomes a signal—and perhaps a strategic one.

Strip away the optics, and what emerges is a group in transition, not retreat. The headline number may suggest softness, but the underlying story is more nuanced: most of Kering’s Houses posted growth, jewelry delivered standout performance, and Gucci—still the gravitational center of the business—is beginning to show early signs of traction in key markets.

The Fashion & Leather Goods division, long the barometer of Kering’s health, declined 3 percent on a comparable basis. Yet within that, there were pockets of strength. Saint Laurent, Bottega Veneta, Balenciaga, and Brioni all delivered growth, with North America emerging as a bright spot. Saint Laurent’s momentum in footwear and ready-to-wear, alongside the rollout of new products like the Mombasa bag, suggests a brand regaining rhythm. Bottega Veneta continues to quietly build on its desirability in Asia-Pacific, supported by a disciplined product pipeline. Even Balenciaga, often a lightning rod for conversation, delivered another quarter of growth on the back of its leather goods business.

Gucci, however, remains the story—and the challenge. Revenues fell 14 percent reported, or 8 percent on a comparable basis, with retail sales down 9 percent. Yet within those numbers sits a more encouraging signal: North America grew 8 percent, offering what the company called “initial confirmation” that the reset is beginning to resonate. It’s not enough yet to offset declines in Asia-Pacific and Western Europe, but it is directionally important.

De Meo has made it clear that Gucci is his top priority, and the actions underway are extensive. “A comprehensive turnaround is underway, with decisive actions across client, distribution and, above all, the offer,” he said. The reset of product architecture, a sharper category focus, and a phased rollout of new collections are designed to rebuild the brand from the inside out. It’s less about a quick fix and more about reestablishing a foundation.

Elsewhere, the story shifts from repair to momentum. Kering Jewelry delivered one of the strongest performances in the group, with revenues up 22 percent on a comparable basis to €269 million. Boucheron led the charge, posting the highest growth within the portfolio, while Pomellato, DoDo, and Qeelin all contributed to a broad-based expansion. In a sector increasingly looking for resilience, jewelry continues to offer it.

Kering Eyewear also marked a milestone quarter, reaching its highest revenue level to date at €489 million, up 7 percent on a comparable basis. Strong product launches, including the first Valentino Eyewear collection developed in-house, alongside effective marketing campaigns, reinforced the division’s role as a consistent growth driver.

Behind the scenes, the group has been just as active. Over the past several months, Kering has executed a series of strategic moves aimed at strengthening its balance sheet and sharpening its focus. The €4 billion sale of Kering Beauté to L’Oréal, alongside the divestment of key real estate assets, signals a clear intent: reduce debt, streamline operations, and refocus on core Houses. De Meo’s broader “ReconKering” strategy, set to be unveiled in Florence at the group’s Capital Markets Day, is expected to build on that foundation.

At the same time, operational changes are underway. The creation of new group platforms designed to enhance efficiency and support brand growth, along with the establishment of internal centers of excellence, points to a more integrated and disciplined organization. It’s a shift from expansion to optimization.

The external environment, however, remains far from stable. Kering noted an 11 percent decline in retail revenue in the Middle East during the quarter, following disruptions tied to the ongoing conflict. While the region represents roughly 5 percent of group retail revenue and the network remains fully operational, the broader concern lies in its potential impact on tourism flows and global consumer sentiment.

And that may be the larger story. Luxury today is not just navigating brand resets, but a world that feels increasingly unpredictable. In that context, Kering’s emphasis on agility and execution feels less like a strategy and more like a necessity.

So where does that leave the group?

Somewhere between stabilization and recovery. Not yet growing, but no longer sliding. A company that has stopped the drift and is beginning, cautiously, to steer again.

For Kering, that may be the most important shift of all.