Regional Shifts And External Pressures Begin To Surface

Hermès delivered another steady quarter for Q1 of 2026, but the more important question isn’t how it performed—it’s what that performance signals about what comes next. Beneath the consistency, the contours of today’s luxury market are becoming clearer.

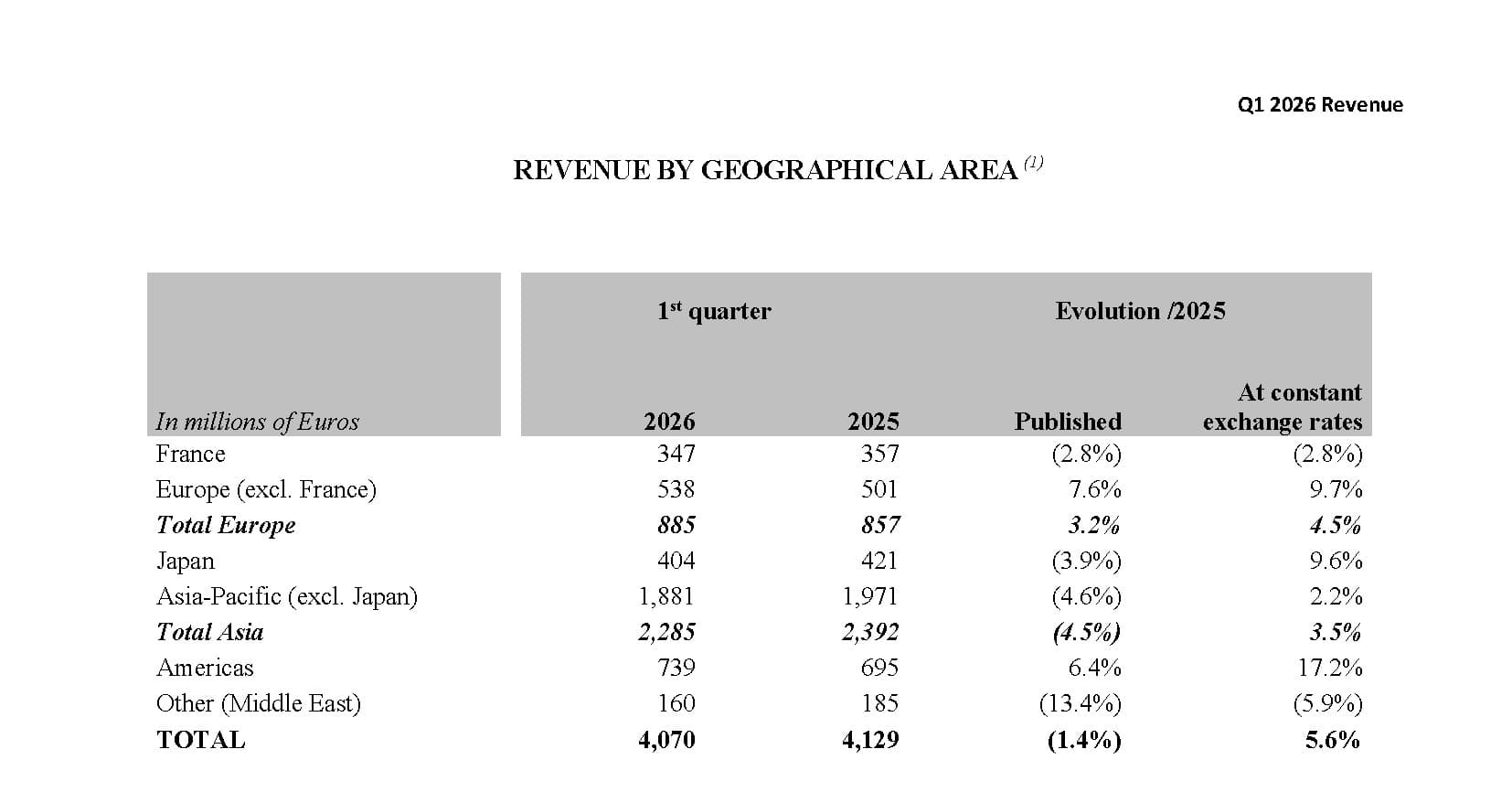

For the first quarter of 2026, the group reported revenues of €4.1 billion, up 6 percent at constant exchange rates, while currency fluctuations pushed reported sales slightly down by 1 percent. The divergence between underlying growth and reported performance is becoming a familiar feature across the sector, but in Hermès’ case it also highlights something more fundamental: demand remains intact, even as external pressures begin to show.

Geographically, performance is becoming more uneven. The Americas led decisively, rising 17 percent at constant exchange rates, while Japan and Europe outside France delivered strong double-digit growth. In each of these regions, the strength was driven primarily by local clients rather than tourism, reinforcing a shift that has been building over the past year.

Asia, by contrast, continues to normalize. Sales in the region excluding Japan grew 2 percent, with Greater China showing only modest improvement. The market has not disappeared, but it is no longer carrying the same weight. Instead, it is settling into a more measured role within the global luxury mix.

The Middle East introduced a more immediate variable. Sales in the region declined as geopolitical tensions disrupted retail operations and travel flows, particularly in March. The impact, while localized, was more acute than the headline number suggests. According to Executive VP of Finance Eric du Halgouët, store closures and reduced operating hours across parts of the United Arab Emirates, Qatar, Bahrain and Kuwait led to sharp daily declines. “Our revenue dropped by 20 to 30 percent depending on the day,” he said. The region ultimately represented about a 1.5 percent impact on the quarter, underscoring how quickly external events can ripple through even the most controlled business models.

The effects extended beyond the region itself. Du Halgouët noted that the disruption also weighed on global tourism, contributing to softer performance in Europe, particularly in Paris. Travel retail was also affected, with roughly 40 of the group’s 60 airport locations experiencing disruption during the quarter. It’s a reminder that while Hermès is often insulated from broader volatility, it is still connected to the same global flows that shape the rest of the industry.

Taken together, these shifts point to a market that is becoming less synchronized and more regionally driven. For Hermès, that changes the nature of growth. It’s no longer about one engine outperforming, but about balancing several—each moving at a different pace.

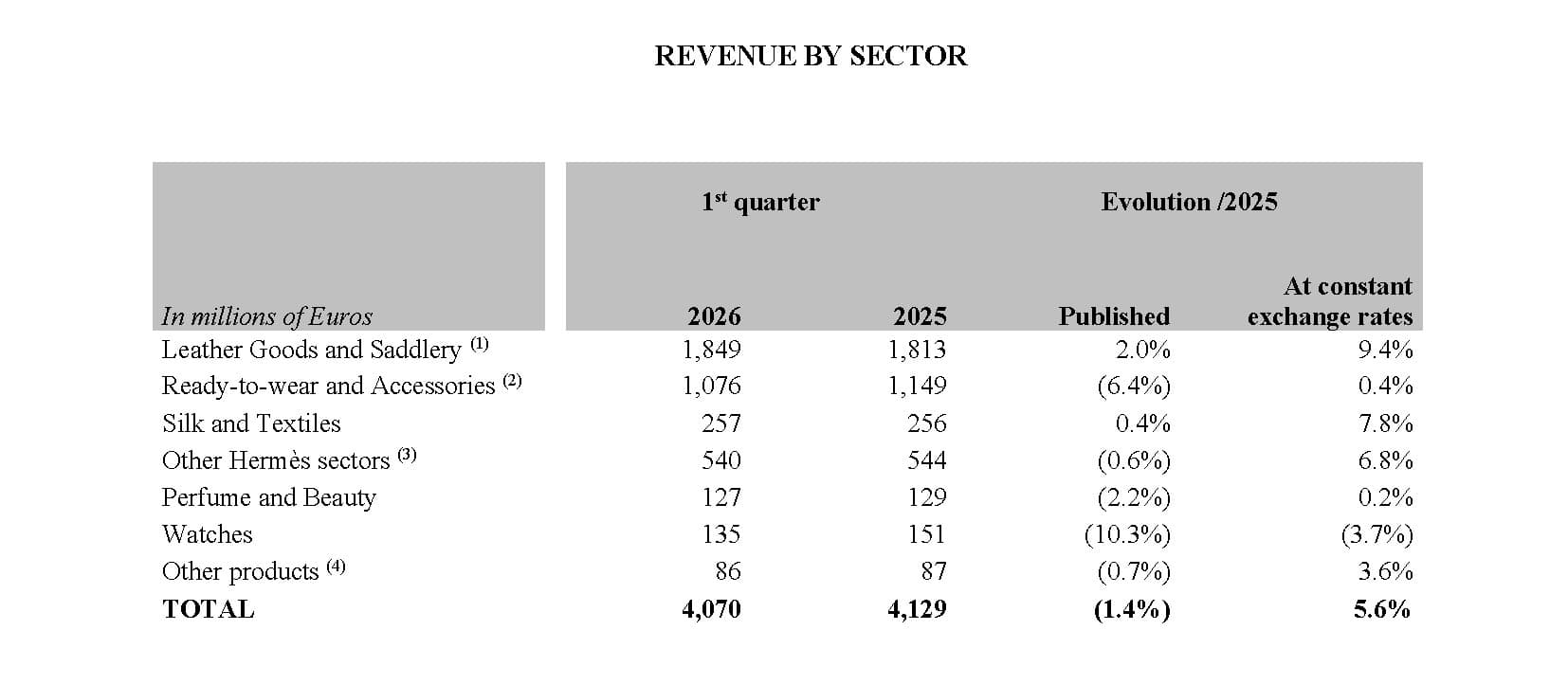

At the product level, Hermès’ core engine remains firmly in place. Leather goods and saddlery grew 9 percent, supported by sustained demand and incremental increases in production capacity. The strategy continues to center on controlled expansion—adding supply carefully while maintaining the brand’s positioning.

At the same time, the group is evolving its offer in quieter ways. “We want to create other bags, not just the Kelly and the Constance,” du Halgouët said, pointing to an ongoing effort to broaden the product base. New designs are tested continuously, with some phased out and others gaining traction over time. It’s a slower, more iterative approach than the seasonal reinventions seen elsewhere, but one that aligns with the house’s long-term philosophy.

That shift may prove more important than it appears. As growth becomes less geographically concentrated, product breadth becomes a more critical lever. Expanding beyond the house’s most iconic lines allows Hermès to capture demand across a wider client base without relying on any single category or region.

Other categories were more mixed. Silk and textiles grew 8 percent, reflecting continued creative renewal, while ready-to-wear and accessories were broadly flat. Watches declined, highlighting the uneven demand environment in more discretionary segments. Even at Hermès, growth is no longer uniform across all categories.

What stands out is less the pace of growth and more the way it is being delivered. Hermès continues to rely on a tightly controlled model—integrated production, disciplined distribution, and a focus on core categories—at a time when much of the sector is still recalibrating pricing and product strategies.

That model remains effective, but the environment around it is becoming more complex. Regional performance is diverging, currency movements are shaping reported outcomes, and geopolitical developments are beginning to influence traffic patterns and consumer behavior in real time.

So what comes next for Hermès is less about acceleration and more about distribution. Growth is likely to come from a broader mix of regions, a wider product base, and incremental increases in capacity—rather than a single breakout driver. It’s a quieter path forward, but arguably a more resilient one.

Looking ahead, Hermès remains confident, but measured. The group continues to invest in production capacity, with new workshops coming online and additional sites planned through 2030. It is also expanding selectively in retail, with approximately 20 store projects in the pipeline globally.

“Our fundamentals remain strong, with great teams out there and loyal clients,” du Halgouët said. The assumption is not that volatility disappears, but that it can be absorbed.

For now, Hermès remains well positioned. But the takeaway from this quarter is not just that the house continues to grow—it’s how that growth is shifting. In a market that is becoming more fragmented and more reactive, Hermès is evolving in a way that is measured, deliberate, and increasingly diversified.

And that may be the real answer to what comes next.