Luca De Meo Lays Out A Structural Reset As The Group Moves To Rebuild Control, Clarity, And Long-Term Growth

Kering arrived in Florence this week with something it has not had in some time: a clear plan—and a quiet acknowledgment that the old one stopped working.

After a decade of expansion, the Group is no longer trying to accelerate. It is trying to reset. ReconKering is less about ambition and more about correction, a shift away from momentum and toward discipline.

The message from the presentation was direct: a model that worked for a decade is no longer effective. That admission shapes everything that follows.

Luca de Meo, Kering CEO, framed the strategy as a bridge between “True Luxury” and “Next Luxury,” but the substance of the plan is grounded in something more immediate. Kering is working to regain control—of its brands, its operations, and ultimately its performance.

The priorities are clear: restore desirability, tighten execution, and simplify the way the Group operates. What stands out is how operational the plan is. The seven core actions outlined focus less on creativity and more on control—inventory, pricing, retail footprint, and organizational structure. This is a reset built on discipline, not reinvention.

Gucci sits at the center of that effort.

The brand remains Kering’s largest asset and its most pressing challenge. The strategy calls for a return to what makes Gucci unmistakable, with clearer codes, a more coherent product architecture, and a more disciplined distribution model.

The reset is necessary, but it also reflects how far the brand had drifted from its own center.

The presentation makes clear that Gucci’s recovery is being treated as structural. SKU reductions of roughly 20 percent, tighter pricing architecture, and a more controlled retail approach are all part of the plan. The goal is not simply to refresh the brand, but to simplify it.

Early signs remain mixed. North America has shown some improvement, but Asia and Europe continue to lag. New collections are arriving, but the market is still waiting for consistent evidence that the product is resonating at scale. The strategy is defined. The timeline remains uncertain.

Across the rest of the portfolio, the approach is more measured.

Saint Laurent is being asked to extend its strengths, particularly in ready-to-wear and menswear, while expanding further into Asia. Bottega Veneta continues to build on its distinctive, understated positioning, extending into a broader wardrobe while maintaining its identity. Balenciaga is being rebalanced, McQueen streamlined, and Brioni further refined at the highest end of tailoring.

For several years, parts of the industry leaned heavily into momentum—newness, visibility, and rapid expansion. Kering’s reset suggests a different approach, one that prioritizes coherence over noise and consistency over bursts of excitement.

Behind the brands sits the more consequential shift.

ReconKering introduces a centralized platform designed to bring greater coordination across industry, client, technology, sustainability, and support functions. The goal is to reduce complexity and improve decision-making, allowing each House to operate with more clarity and consistency.

That discipline extends to the physical network. Kering plans to close more than 100 stores while renovating much of the rest, alongside a structural reduction in inventory. The focus is shifting from scale to quality—fewer stores, stronger productivity, and clearer positioning.

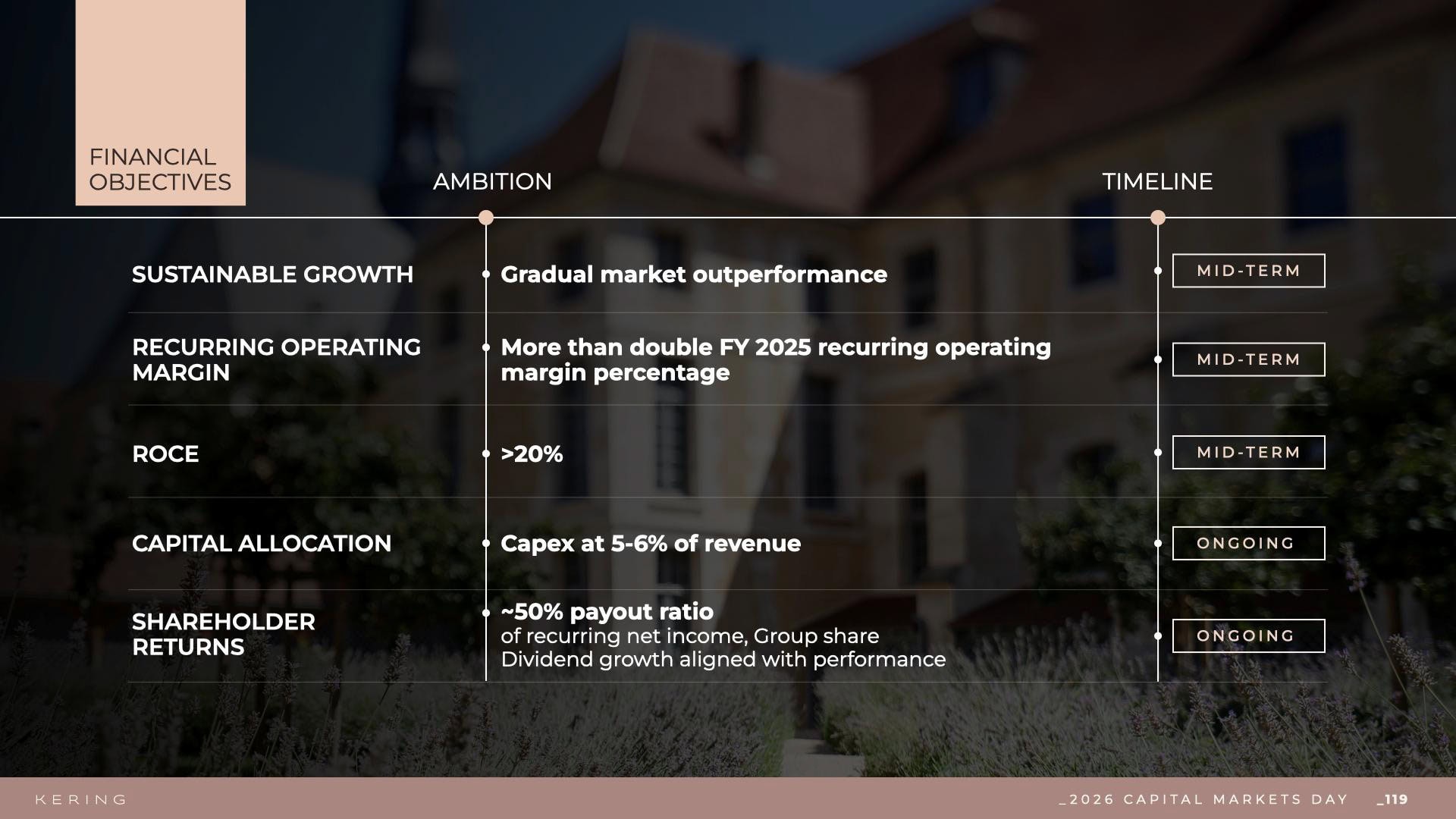

The financial ambitions reflect the scale of the reset. The Group is targeting a more than doubling of its operating margin over the mid-term, alongside improved capital efficiency and more selective investment. These targets are not about incremental improvement. They require a meaningful change in how the business performs.

The roadmap is structured across three phases: reset by the end of 2026, rebuild through 2028, and reclaim leadership by 2030. It is a long horizon, but one that reflects how much needs to be rebuilt.

What stands out most is the tone.

De Meo described Kering as a challenger. It is a notable shift for a Group that once led the conversation. The advantage of that position is that it allows for a more disciplined approach—one focused less on expectation and more on execution.

Because that is where this plan will be judged.

Kering is not trying to outpace the market. It is trying to regain control of its business.

That is a different kind of ambition, and a more difficult one to deliver. In a market that has become less forgiving, growth built on discipline may prove more durable than growth built on momentum.